Estimated reading time: 14 minutes

Every investor goes through this at least once. You spend weeks watching a stock, finally pull the trigger, and the very next day it drops 10%. You panic, sell, and then watch it rocket past your original entry price like it was waiting for you to leave. It almost feels personal.

Here’s the uncomfortable truth: someone really is shaping the price you see on your screen. Not targeting you specifically, but moving the market in ways most retail investors never account for. These are the big institutions, hedge funds, fund managers, pension funds, they are collectively moving trillions of dollars across global markets every single day. The financial world calls them smart money.

And here’s the interesting part: by law, most of these institutions are required to publicly disclose what they are buying and selling. Which means anyone with a phone can technically see exactly what the world’s biggest investors are doing. For free.

So why are retail investors still losing?

TABLE OF CONTENTS

- Why Retail Investors Actually Lose

- What Is “Smart Money,” Really?

- A Four-Step Investigation Framework

- Step 1: Is Smart Money Actually Serious?

- Step 2: Do Professional Analysts Still Believe in It?

- Step 3: Are the Company’s Own Insiders Backing It?

- Step 4: Does the Actual Business Hold Up?

- The Full Picture

- Final Thoughts

Why Retail Investors Actually Lose

It’s rarely about picking a “bad” stock. The more common culprit is when and why people buy and sell.

The pattern tends to look like this:

- Buying after the hype has already peaked.

Take Malaysian glove stocks in 2020. By the time most retail investors were buying Top Glove or Hartalega, after it was all over WhatsApp groups and family chats, smart money had already been holding for months. Retail investors weren’t early. They were the exit liquidity.

- Panic selling on dips.

The stock drops, anxiety sets in, and shares get sold. Then it recovers without you.

- Confusing rising prices with a good business.

Glove stocks climbed for months while the underlying business was quietly becoming a worse long-term bet, as global demand was tied to a pandemic that was eventually going to end.

The real gap isn’t intelligence or luck. It’s information and timing. Institutions plan their moves months in advance, backed by dedicated research teams. Retail investors react in real time, emotionally, and usually too late.

The goal, then, is to stop reacting blindly and start reading what the planners are actually doing.

What Is “Smart Money”?

The term gets thrown around loosely, so it helps to be specific. Smart money generally refers to three groups:

- Institutional investors – pension funds like EPF or KWAP locally, or Berkshire Hathaway in the US

- Hedge funds – professionally managed pools of capital with aggressive return targets

- Company insiders – the CEOs, CFOs, and directors who run the business day to day

These groups have more resources, information, and patience than the average retail investor. But, and this matters, having an edge doesn’t mean they’re always right. Blindly copying their moves, without understanding the reasoning behind them, is one of the fastest ways to lose money.

EPF, KWAP, and major foreign funds were all holding Malaysian glove stocks near the peak. The Serba Dinamik governance scandal caught institutional holders completely off guard. Smart money got it wrong, and so did everyone who simply copied them without doing their own thinking.

So smart money signals are a starting point, not a conclusion. The question is how to use them properly.

A Four-Step Investigation Framework

The right way to think about smart money is as one input in a structured process, not a shortcut that replaces research. Here’s the four-question framework used before committing to any position:

- Is the smart money actually serious about this stock?

- Do professional analysts still believe in it?

- Are the company’s own insiders backing it?

- Does the actual business hold up?

Every question has to pass before moving to the next. If a stock fails even one, walk away. This walkthrough uses Alphabet (Google’s parent company) as the example, using Moomoo‘s built-in tools , which handle most of the data gathering automatically.

Step 1: Is Smart Money Actually Serious?

When a big fund holds a stock, the first question isn’t what they hold, it’s how much they care about that position.

A RM10 million position means nothing to a fund managing RM50 billion. Copying a stock that represents 0.02% of their portfolio means copying a decision they barely considered. What matters is conviction, a position large enough that it actually moves the needle for them, and ideally, one they’re actively adding to rather than quietly trimming.

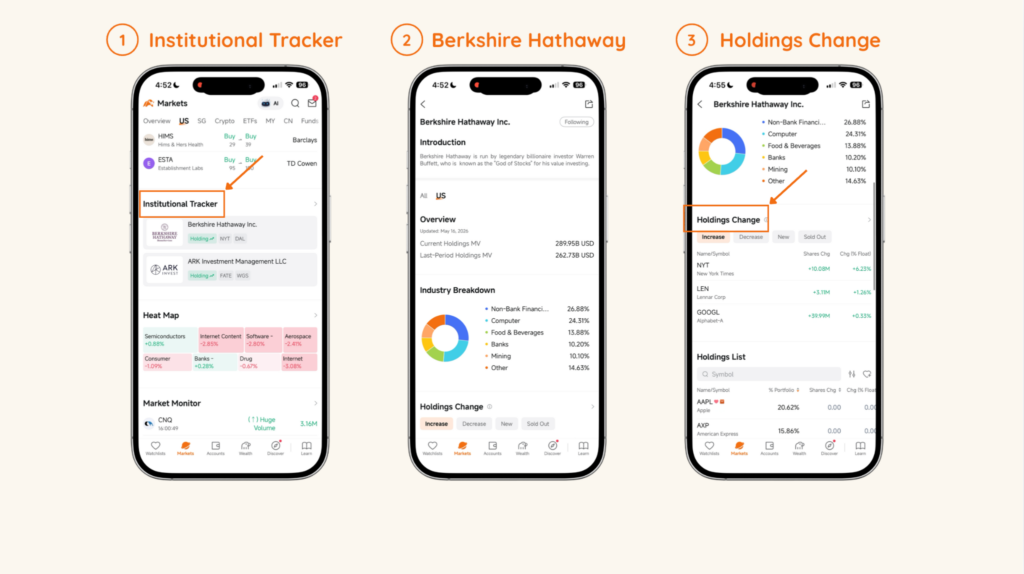

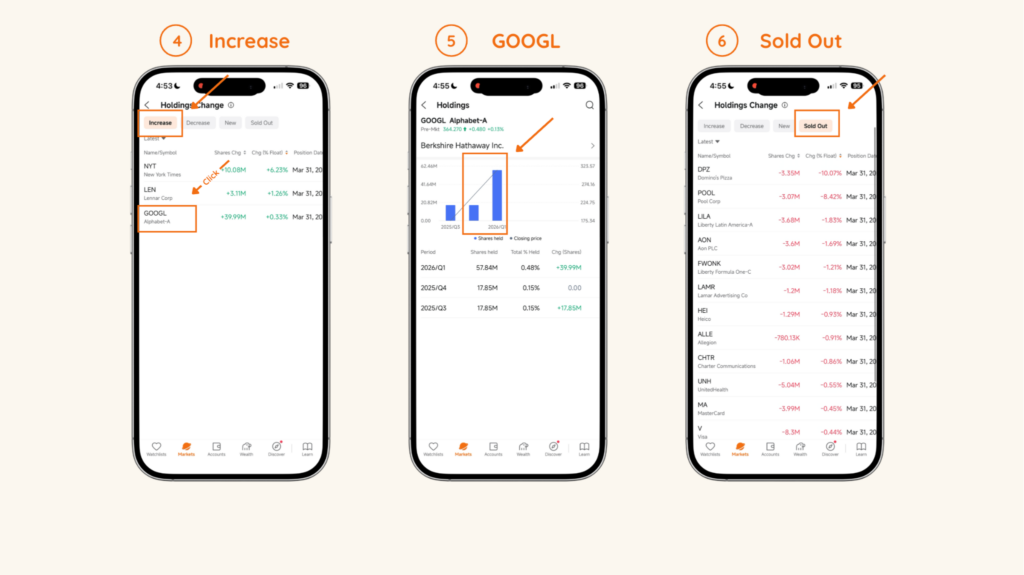

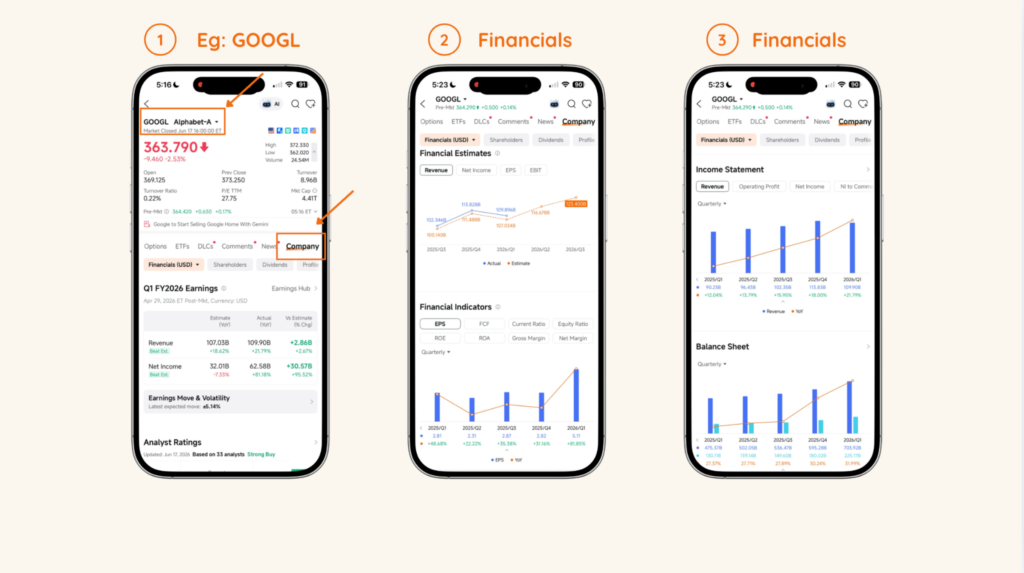

Moomoo‘s Institution Tracker makes this visible. For any major institution, users can see their full portfolio breakdown: what they bought, what they sold, and what percentage each position represents.

On 15 May 2026, Berkshire Hathaway filed its Q1 2026 13F report, the first under new CEO Greg Abel, after Warren Buffett officially stepped down at the start of 2026. Abel’s first filing was notable. He increased Berkshire’s Alphabet (GOOGL) position by 224%, from roughly 18 million shares to nearly 58 million shares, while fully exiting Amazon, Domino’s, and UnitedHealth.

That is not a casual position adjustment. When a new CEO’s very first major filing triples down on a single name, it reflects high conviction from the most watched institutional portfolio in the world.

Alphabet passes Step 1.

Here’s how you can explore the Institutional Tracker yourself on Moomoo app:

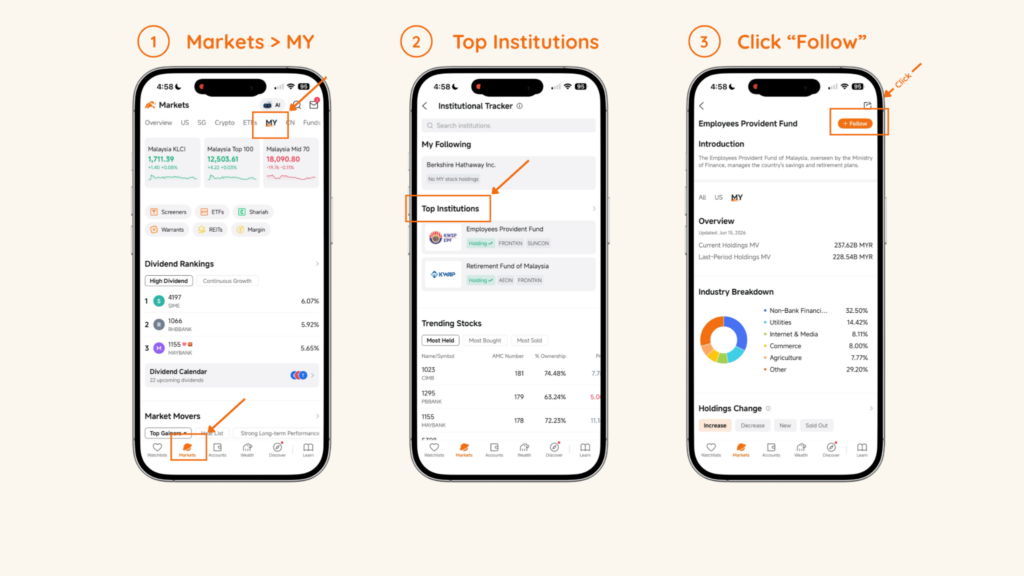

A practical tip: Moomoo‘s Institution Tracker also covers local institutions like EPF and KWAP on Bursa, not just US funds. The “Follow” feature sends a notification the moment a new disclosure is filed, so instead of reading about it days or weeks later in the news, the update arrives the same day.

For tracking faster-moving players like politically connected portfolios or prominent individual investors, the Insight Page covers names that don’t show up in regular 13F filings.

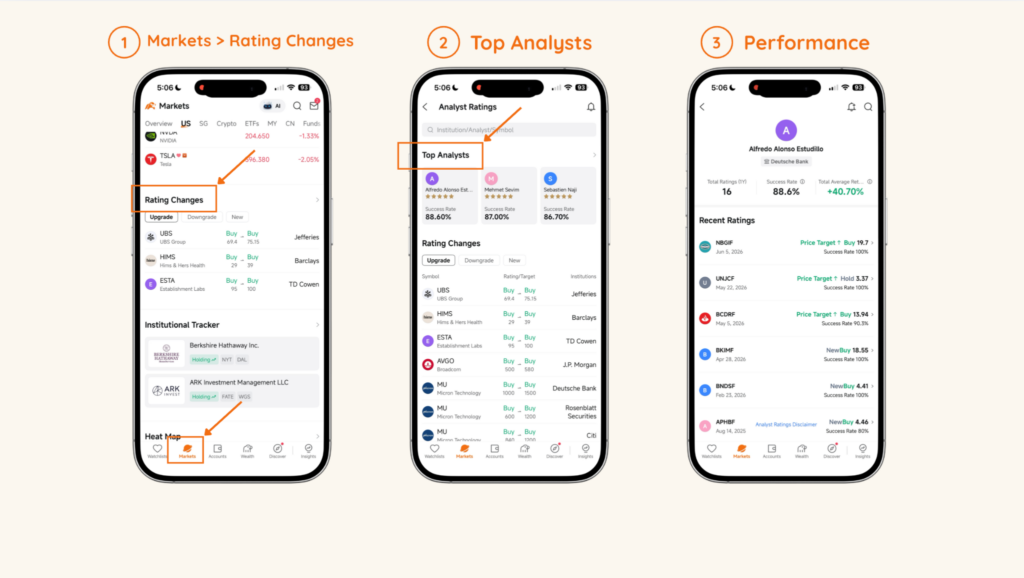

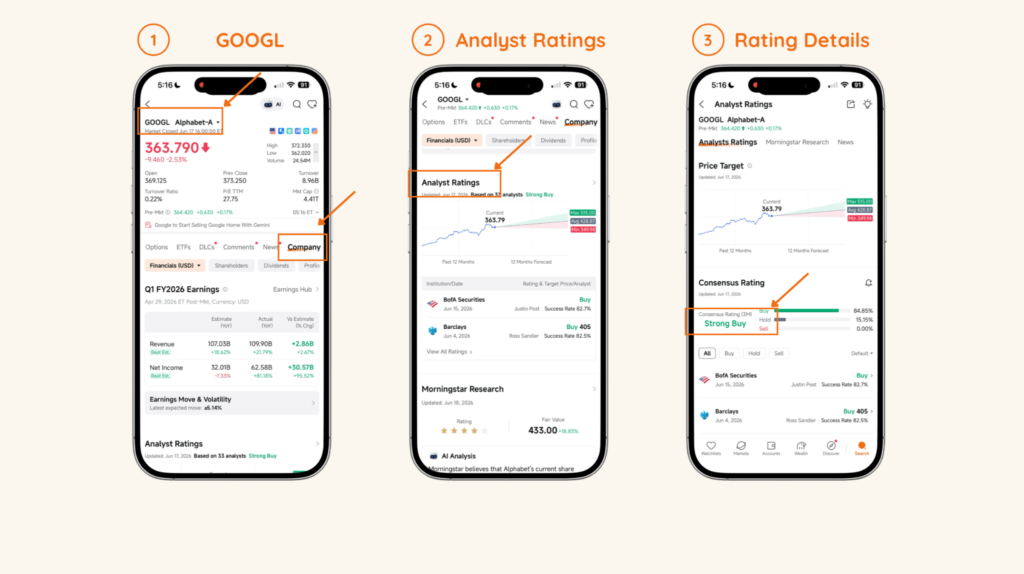

Step 2: Do Professional Analysts Still Believe in It?

Here’s the problem with Step 1: that 13F filing reflects what the fund held at the end of the previous quarter. By the time it’s visible, the data can be up to 45 days old. Smart money may have bought Alphabet months ago at a much lower price. The real question is whether it still makes sense at today’s price, or whether the opportunity has already passed.

That’s what analyst ratings are designed to answer.

Major investment banks like Goldman Sachs, Morgan Stanley, JP Morgan globally; CIMB Research, Maybank IB, and MIDF locally, publish research reports with target prices and Buy / Hold / Sell ratings. The challenge is that for any single stock, 20 different analysts might give 20 different opinions, with wildly different target prices.

Moomoo solves this by assigning each analyst their own Star Rating based on actual historical track record: how often their calls were right, how accurate their price targets were, and how the recommended stocks actually performed afterward. A Buy rating from a 5-star analyst carries meaningfully more weight than the same rating from a 1-star one.

Step to Use Moomoo’s Rating Changes:

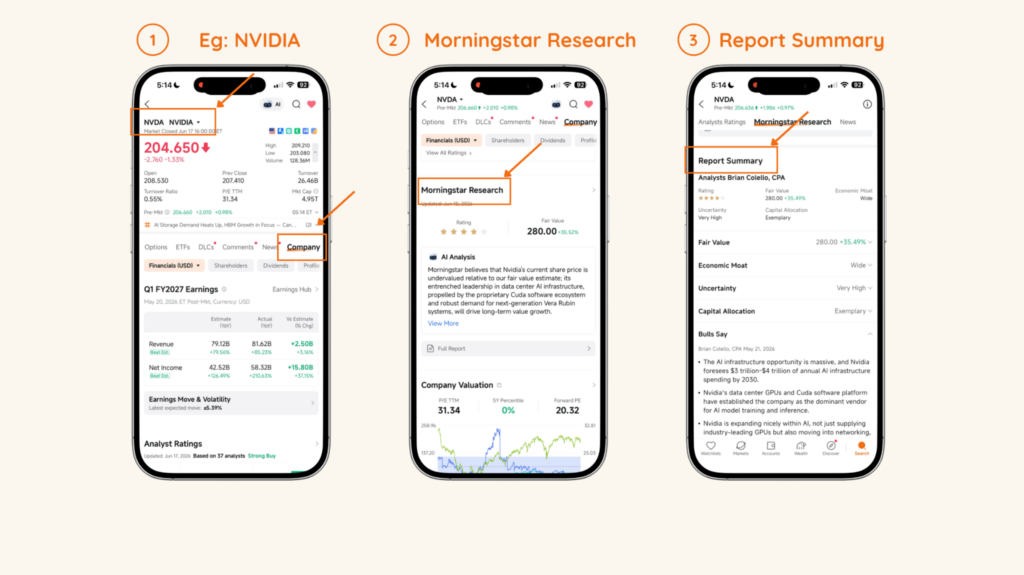

Moomoo also includes Morningstar ratings at no extra cost, one of the most respected independent research houses in the world, whose reports normally require a paid subscription.

Running Step 2 on Alphabet: if multiple high-rated analysts still carry upside targets above today’s price, the conclusion is that professional opinion hasn’t soured since the institutional buying happened. The conviction is current, not just historical.

Alphabet passes Step 2.

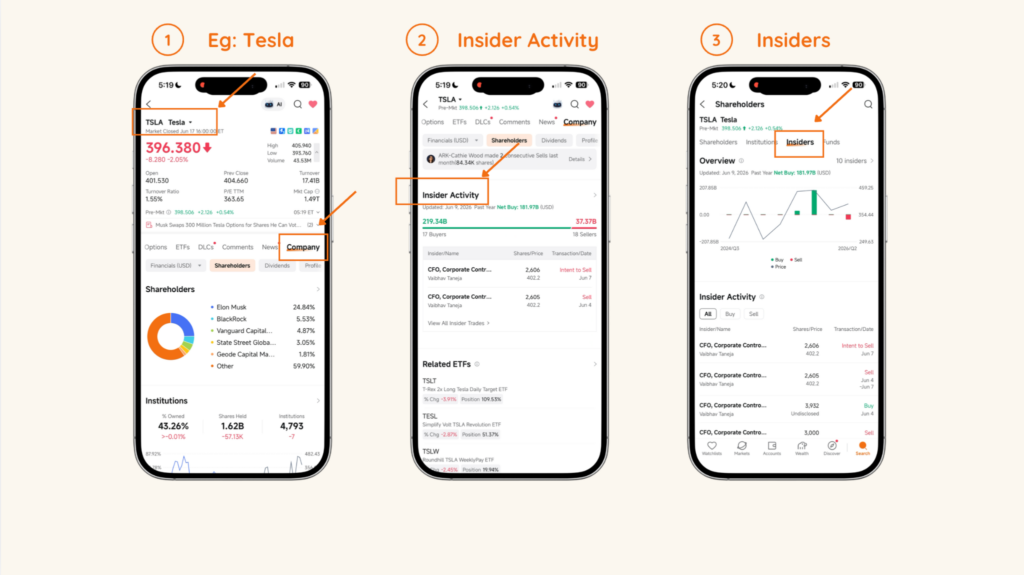

Step 3: Are the Company’s Own Insiders Backing It?

No one knows more about where a company is actually headed than the people running it. When a CEO, CFO, or director uses their personal money to buy shares in their own company, it’s one of the most honest signals available in public markets. Nobody voluntarily puts money into a sinking ship.

In Malaysia, directors and substantial shareholders are required to declare any share purchases or sales within three days. In the US, these are filed as Form 4 with the SEC. The information is public, but it’s buried across hundreds of company filings, and most retail investors never look at it.

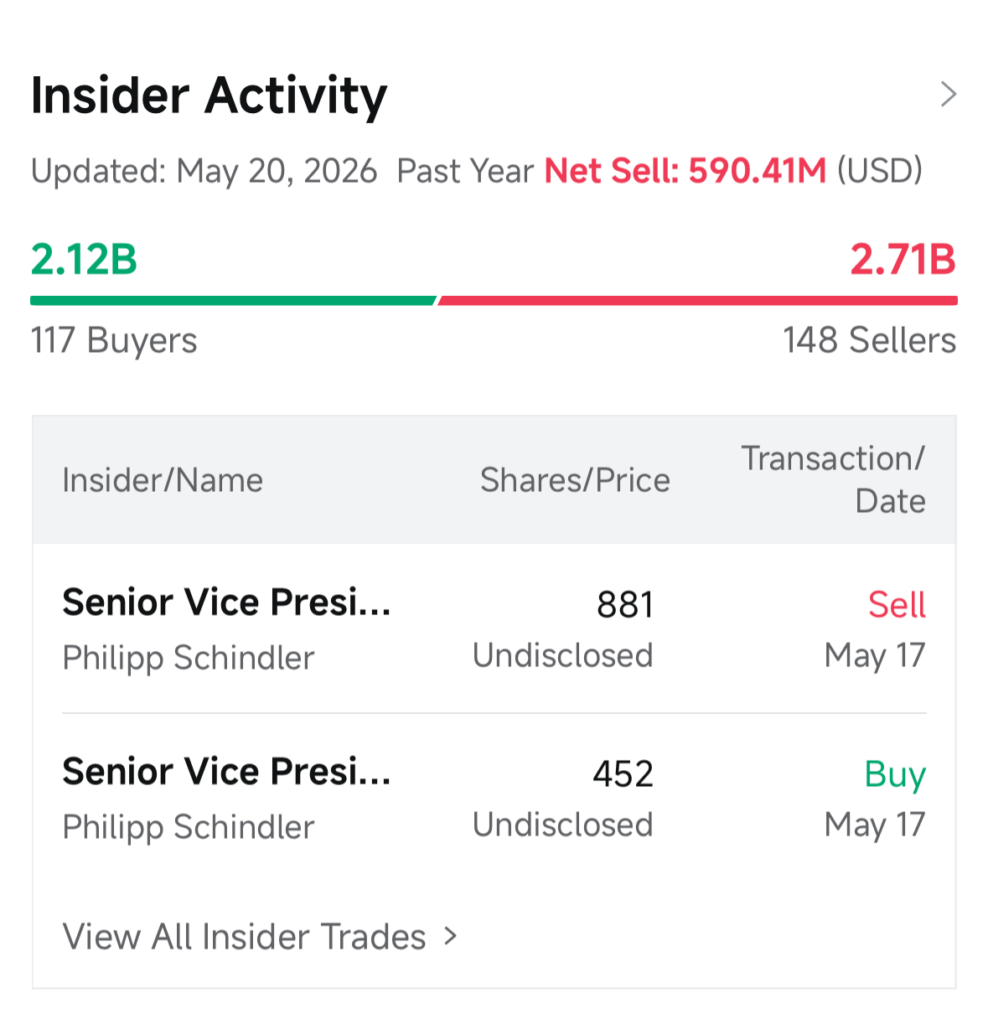

Moomoo‘s Insider Activity section consolidates all of this into a simple dashboard: the number of insiders buying versus selling, and the total dollar amounts involved.

Step to Use Moomoo’s Insider Activity:

For the Alphabet, the picture isn’t a clean green light. As at 20 May 2026, over the past year, insiders were net sellers, roughly USD 590 million more in sales than purchases, with 148 sellers versus 117 buyers.

The instinct might be to treat this as a red flag. But insider selling requires more careful interpretation than insider buying.

When an executive buys shares with personal money, there’s essentially one reason: they believe the price is going up. Buying is a strong, unambiguous signal. Selling, on the other hand, has dozens of mundane explanations, such as funding a home purchase, estate planning, diversifying personal wealth, or simply managing the fact that most senior executives are paid heavily in company equity and periodically need to convert some of it to cash.

The signal to watch for isn’t any selling, it’s heavy, one-sided selling. Ten sellers and zero buyers. A mass exodus of insiders heading for the exits simultaneously. That’s the pattern that should stop an investigation cold.

That’s not what the Alphabet shows. The activity is split, not a stampede. For a company of this scale, with thousands of employees holding share-based compensation, that ratio is fairly normal.

Alphabet passes Step 3, but with a note. Not a clean green light; more of a “proceed, but stay alert.” That’s how many real investigations end on this question. The signals don’t always line up perfectly. The job is to weigh them accurately, not wait for a scenario where everything is flawless.

Step 4: Does the Actual Business Hold Up?

This is where most investors get into trouble. Three positive signals come in, and they buy, without ever asking whether the underlying company actually makes money.

A stock is not a story or a sentiment score. It is a piece of ownership in a real business, and sooner or later, the numbers are what determine the outcome.

This final step is a fundamental health check, and it only requires five questions:

- Is revenue growing?

- Are profit margins stable, or being squeezed?

- Is debt manageable?

- Does the company pay a consistent dividend, and is it sustainable?

- Is the valuation (PE ratio) reasonable compared to peers, or is the current price mostly hype?

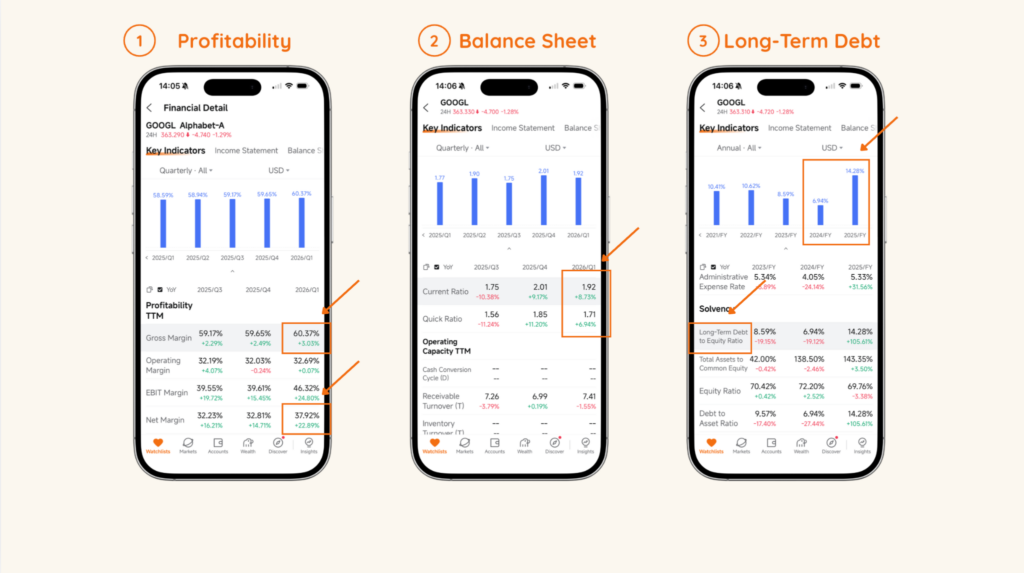

Step to Use Moomoo’s Company Financials:

Running this on Alphabet in Q1 2026:

Profitability is exceptional. Gross margin has climbed steadily, reaching around 60%. Net margin hit nearly 38%, meaning for every USD 100 in revenue, approximately USD 38 is pure profit. Most businesses spend careers chasing margins like that.

The balance sheet is solid. A current ratio of 1.92 and quick ratio of 1.71 both sit comfortably above 1.0, meaning the company has more than enough liquid assets to cover its short-term obligations without stress.

Debt is increasing, and worth watching. Long-term debt moved from roughly 7% in 2024 to around 14% in 2025. In absolute terms, this remains low for a company of Alphabet’s scale, likely driven by AI infrastructure and data centre investment. It is not a red flag today, but the direction of travel is something to note and monitor. Ignoring small cracks because the broader story is appealing is how investors get surprised.

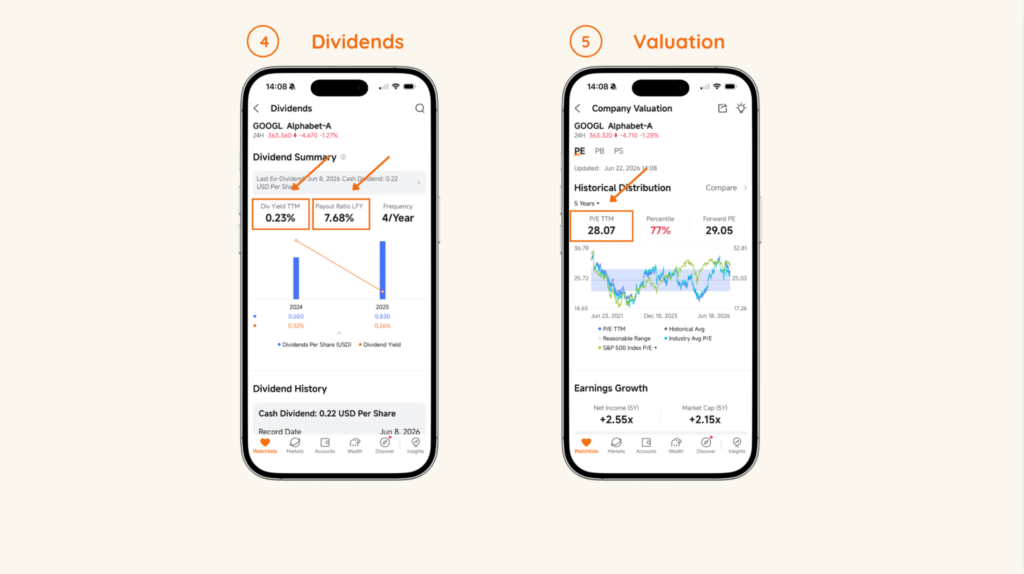

Dividends are minimal. The yield is just 0.23%, and the company pays out only around 8% of profits. Alphabet is not an income stock. But for a growth company that reinvests the vast majority of its earnings back into the business, this is entirely appropriate, the investment case is capital appreciation, not dividend income.

Valuation is not cheap. The PE ratio sits around 30, which is above the industry average. This means buyers today are paying a premium for future earnings. The business quality justifies a premium, but it is worth acknowledging that the current price does not represent a bargain.

Alphabet passes Step 4, with eyes open. The business is growing, highly profitable, and financially sound. But it is priced as a quality company, not an overlooked one, and debt is quietly trending upward.

The Full Picture

Four questions. Four passes, each with appropriate caveats.

Smart money serious: pass. Analysts are still convinced at today’s price: pass. Insiders mixed, but no sign of mass exits: pass, with a note. Business fundamentally strong: pass, with eyes open.

What’s worth noticing is that none of those four steps required predicting the future. No crystal ball, no insider information, no speculation about macro trends. Just a disciplined process of reading what is already publicly available, and asking the right questions in the right order.

This is how to stop being other people’s exit liquidity, not by finding a hot tip, but by doing the work that most people skip.

Final Thought

Even after completing all four steps on a stock that passes cleanly, the worst mistake is concentrating too heavily on a single name. No matter how strong the signals look, position sizing and diversification matter. Even the world’s most famous investor spreads across dozens of companies.

Investing is also a long-term game. Short-term prices do whatever they want, often for reasons that have nothing to do with business quality. The investors who consistently come out ahead are rarely the ones who time entries perfectly, they’re the ones who show up consistently, month after month, through both good and bad markets.

Please note that everything covered here is a framework, not a guarantee. It shifts the process from chasing trends to actually understanding what is inside the businesses being considered. And that, over time, is the real edge.

If you want to try all these tools yourself, click here to sign up for a Moomoo account to get extra rewards using my special deposit code “ZIET 11”. They are now giving away US stocks, up to RM1,800 worth of Apple stock plus RM 100 cash for new users. Thanks for reading!

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Always conduct your own research and only invest money you can afford to lose.

Share the Wealth

Found this information useful? Share this post with your friends and family to help them stay informed about what’s happening around them. And if you’re not already subscribed, join our community to receive more insightful content directly to your hands.